Resilient for Now: The UK withstands early Middle East shocks, but fragility and risks remain

Our latest quarterly update suggests the UK economy has so far absorbed the initial shocks from the Middle East conflict without tipping into outright recession or triggering a fresh, energy-led inflation surge. That resilience is reflected in a small uptick in economic confidence and in consumers’ self-assessed finances in our Q3 Outlook, after three quarters of decline. Yet the improvement is only tentative. As higher fuel and energy prices tied to the conflict feed through the economy during the second half of 2026, we could witness delayed inflationary pressures. Consumer behaviour also shows households are not yet convinced enough to increase spending significantly.

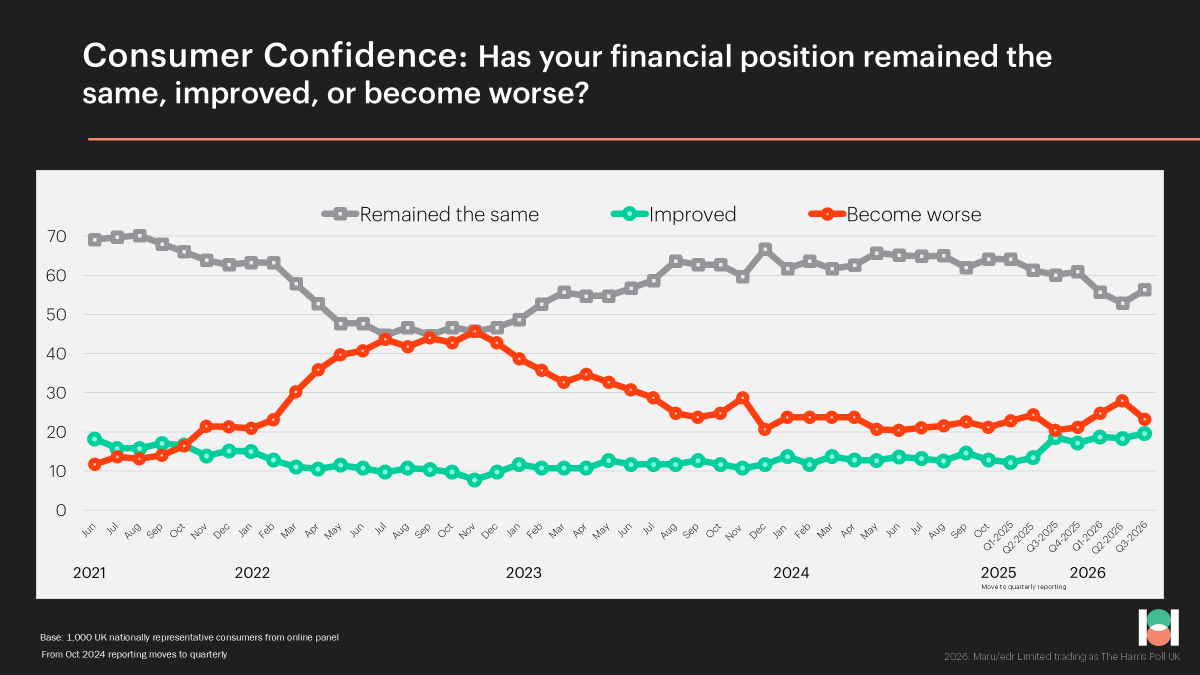

Consumer Confidence has edged up, signalling a tentative improvement in sentiment

Going into Q3, our UK data reports a slight improvement in economic sentiment and personal finances. Importantly, the key indicators show the UK has not experienced the same immediate shock effect that followed the Pandemic or war in Ukraine, which is an encouraging sign that markets and households have been resilient, and so far, absorbed supply and price volatility without a collapse in confidence. However, higher fuel and energy costs linked to the conflict will eventually work their way through the UK economy during the second half of 2026, bringing the risk that price pressures could intensify later in the year as these costs feed through transport, commodity and retail channels. In short: resilience for now, but vulnerability ahead if energy‑linked inflation materialises. The Bank of England has decided to maintain interest rates at current levels, indicating they expect inflationary pressures ahead.

Consumer spending behaviour remains cautious, particularly for discretionary items

Crucially, the marginal uplift in consumer sentiment has not converted into stronger consumer spending. Despite an improving trend, only around one in five UK adults say their personal finances are improving, and intention to make big‑ticket purchases remains muted. This is indicative of the real-life choices for many consumers, with the majority feeling no better off in the last few years. Roughly 70% say they are holding off on major purchases through 2026. This figure has remained at a similar level since the start of the year and day‑to‑day retail spending intentions are similarly flat. This disconnect between sentiment and behaviour suggests consumer‑led growth will remain suppressed and unlikely to drive economic growth in H2 2026. In short, whilst households look a little more optimistic, they are not yet changing behaviour in ways that would materially boost UK growth. For businesses, the implication is a slow and uneven recovery in demand, with compelling all-round value propositions likely required to convert cautious intent into actual transactions.

A change of UK prime minister brings political uncertainty with new policy decisions

Yet another new Prime Minister in the UK introduces a further source of near-term uncertainty. Political transitions typically introduce uncertainty that can weigh on confidence and delay business and household decisions. At the same time, leadership change opens the door for new policy initiatives aimed at stimulating growth. With Andy Burnham increasingly likely to lead the government, markets and households will be especially attentive to early policy signals, not least because it remains unclear what “Burnhamism” will mean in practice for fiscal priorities, public investment and targeted household support. Clear, credible early measures could help convert tentative sentiment into tangible economic momentum; mixed signals or inability to act could deepen caution.

The UK economy is resilient for now, showing a modest improvement in consumer sentiment without immediate collapse. But elevated energy costs, cautious household behaviour and looming political change mean this resilience remains fragile. The next quarter will be critical in determining whether improvements in consumer confidence and economic growth solidify or give way to renewed price pressures and instability driving a continued sluggish performance of the UK economy.

The UK economy and consumers have shown resilience in the face of global uncertainty, creating an opportunity for brands and businesses to build on these early signs of improving sentiment and avoid consumers slipping into 'wait and see' mode.

The Harris Poll UK will continue to track how consumer confidence, spending intentions and economic sentiment evolve over the coming months as households and businesses respond to changing economic conditions.